Wind energy is poised to eventually be the dominant source of power in the United States.

As companies ramp up their workforce to support activities related to wind farm construction and maintenance, it’s critical to understand the various workers’ compensation laws that impact this sector. In this webcast, our Dan Bookham joins colleagues from American Equity Underwriters to discuss:

The various workers’ compensation laws that impact the wind energy sector

Jurisdiction issues unique to offshore wind farms

Old laws that will be interpreted to meet new circumstances

Although 2020 has been a year of unexpected changes, one routine has remained consistent: the fourth quarter means it’s time to begin organizing your finances for the new year. To help you get started, here’s a checklist of key topics to think about, including new tax and retirement considerations related to the COVID-19 pandemic.

1) Max out retirement contributions.

Are you taking full advantage of your employer’s match to your workplace retirement account? If not, it’s a great time to consider increasing your contribution. If you’re already maxing out your match or your employer doesn’t offer one, boosting your contribution to an IRA could still offer tax advantages. Keep in mind that the SECURE Act repealed the maximum age for contributions to a traditional IRA, effective January 1, 2020. As long as you’ve earned income in 2020, you can contribute to a traditional IRA after age 70½—and, depending on your modified adjusted gross income (MAGI), you may be able to deduct the contribution.

2) Refocus on your goals.

Did you set savings goals for 2020? Evaluate how you did and set realistic goals for next year. If you’re off track, we’d be happy to help you develop a financial plan.

3) Spend flexible spending account (FSA) dollars.

If you have an FSA, note that the Internal Revenue Service (IRS) relaxed certain “use or lose” rules this year because of the pandemic. Employers can modify plans through the end of this year to allow employees to “spend down” unused FSA funds on any health care expense incurred in 2020—and let you carry over $550 to the 2021 plan year. If you don’t have an FSA, you may want to calculate your qualifying health care costs to see if establishing one for 2021 makes sense.

4) Manage your marginal tax rate.

If you’re on the threshold of a tax bracket, you may be able to put yourself in the lower bracket by deferring some of your income to 2021. Accelerating deductions such as medical expenses or charitable donations into 2020 (rather than paying for deductible items in 2021) may have the same effect.

Here are a few key 2020 tax thresholds to keep in mind:

The 37 percent marginal tax rate affects those with taxable incomes in excess of $518,400 (individual), $622,050 (married filing jointly), $518,400 (head of household), and $311,025 (married filing separately).

The 20 percent capital gains tax rate applies to those with taxable incomes in excess of $441,450 (individual), $496,600 (married filing jointly), $469,050 (head of household), and $248,300 (married filing separately).

The 3.8 percent surtax on investment income applies to the lesser of net investment income or the excess of MAGI greater than $200,000 (individual), $250,000 (married filing jointly), $200,000 (head of household), and $125,000 (married filing separately).

5) Rebalance your portfolio.

Reviewing your capital gains and losses may reveal tax planning opportunities; for example, you may be able to harvest losses to offset capital gains.

6) Make charitable gifts.

Donating to charity is another good strategy worth exploring to reduce taxable income—and help a worthy cause. Take a look at various gifting alternatives, including donor-advised funds.

7) Form a strategy for stock options.

If you hold stock options, be sure to develop a strategy for managing current and future income. Consider the timing of a nonqualified stock option exercise based on your estimated tax picture. Does it make sense to avoid accelerating income into the current tax year or to defer income to future years? If you’re considering exercising incentive stock options before year-end, don’t forget to have your tax advisor prepare an alternative minimum tax projection to see if there’s any tax benefit to waiting until January.

8) Plan for estimated taxes and required minimum distributions (RMDs).

Both the SECURE and CARES acts affect 2020 tax planning and RMDs. Under the SECURE Act, if you reached age 70½ after January 1, 2020, you can now wait until you turn 72 to start taking RMDs—and the CARES Act waived RMDs for 2020. If you took a coronavirus-related distribution (CRD) from a retirement plan in 2020, you’ll need to elect on your 2020 income tax return how you plan to pay taxes associated with the CRD. You can choose to repay the CRD, pay income tax related to the CRD in 2020, or pay the tax liability over a three-year period. But remember: once you elect a strategy, you can’t change it. Also, if you took a 401(k) loan after March 27, 2020, you’ll need to establish a repayment plan and confirm the amount of accrued interest.

9) Adjust your withholding.

If you think you may be subject to an estimated tax penalty, consider asking your employer (via Form W-4) to increase your withholding for the remainder of the year to cover the shortfall. The biggest advantage of this is that withholding is considered to be paid evenly throughout the year instead of when the dollars are actually taken from your paycheck. You can also use this strategy to make up for low or missing quarterly estimated tax payments. If you collected unemployment in 2020, remember that any benefits you received are subject to federal income tax. Taxes at the state level vary, and not all states tax unemployment benefits. If you received unemployment benefits and did not have taxes withheld, you may need to plan for owing taxes when you file your 2020 return.

10) Review your estate documents.

Review and update your estate plan on an ongoing basis to make sure it stays in tune with your goals and accounts for any life changes or other circumstances. Take time to:

Check trust funding

Update beneficiary designations

Take a fresh look at trustee and agent appointments

Review provisions of powers of attorney and health care directives

Ensure that you fully understand all of your documents

Be Proactive and Get Professional Advice

Remember to get a jump on planning now so you don’t find yourself scrambling at year-end. Although this list offers a good starting point, you may have unique planning concerns. As you get ready for the year ahead, please feel free to reach out to us to talk through the issues and deadlines that are most relevant to you.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.

In the Spring 2018, I wrote about Financial Wellness in general, and how good financial planning and cash-flow management can support overall health and well-being. A lot has changed in the past two years, and the topic is more relevant than ever.

Given what many are calling the most severe economic downturn since the Great Depression in the wake of the pandemic, I would like to explore what often become the most significant issues for people facing a financial crisis – and how to build resiliency to downturns – drawing on material published by our colleagues at Commonwealth Financial Network (CFN).

Debt. Generally, people carry some amount of debt: a student loan, mortgage, or car loan. It can be financially smart to make a large purchase using someone else’s money. Borrowing allows one to purchase big-ticket items with less out-of-pocket cash. And, with today’s attractive interest rates, at a relatively low cost. Taking on any amount of debt comes with risk; A financial setback can reduce your ability to repay a loan, and debt may prevent taking advantage of other financial opportunities.

How Much Debt is OK?

Take a close look at your personal finances, focusing on the following factors:

Liquidity. If there is anything many people have learned in 2020 is that it’s a good idea to maintain an emergency fund to cover three to six months’ worth of expenses. CFN warns us to guard against keeping more than 120 percent of your six-month expense estimate in low-yielding investments. And don’t let more than 5 percent of your cash reserves sit in a non-interest-bearing checking account.

Current debt. CFN also stresses that total monthly debt payments like mortgages should not exceed 36 percent of monthly gross income. Consumer debt payments—credit card balances, automobile loans and leases, and debt related to other lifestyle purchases—they also say should total less than 10 percent of your monthly gross income. If your consumer debt ratio is 20 percent or more, avoid taking on additional debt.

Housing expenses. Monthly housing costs—including mortgage or rent, home insurance, real estate taxes, association fees, and other required expenses—shouldn’t amount to more than 31 percent of monthly gross income, according to CFN. Lenders use their own formulas to calculate how much home you can afford based on your gross monthly income, your current housing expenses, and your other long-term debt, such as auto and student loans. For a mortgage insured by the Federal Housing Administration (FHA), your housing expenses and long-term debt should not exceed 43 percent of your monthly gross income. With mortgage interest rates dropping to historic lows, many are refinancing or considering refinancing. If you are in the first few years of your existing mortgage, this can make sense, or if you would like to reduce payments to improve cash flow, this can be a great strategy. If you’re close to paying off your mortgage, however, it may not make sense given how the interest portion of payments are smallest as the mortgage reaches maturity.

Evaluating Mortgage Options. If you’re in the market for a new home, the myriad of mortgage choices can be overwhelming. Fixed or variable interest rate? Fifteen- or thirty-year term? If it were merely a question of which mortgage provided the lowest long-term costs, the answer would be simple. In reality, the best mortgage for a particular household depends on how long the homeowner plans to stay in the house, the available down payment, the predictability of cash flow, and the borrower’s tolerance for fluctuating payments.

How long will you be in that home? One rule of thumb is to choose a mortgage based on how long you plan to stay in the home. If you plan to stay 5 years or less, consider renting. If you plan to live in the house for 5 to 10 years and have a high tolerance for fluctuating payments, consider a variable-rate mortgage for a longer term, such as 30 years, to help keep the cost down. If the home is a long-term investment, choose a fixed-rate mortgage with a shorter term, such as 15 or 20 years.

Is a variable-rate mortgage worth the risk? Keep in mind that it’s generally not wise to take on a variable-rate mortgage simply because you qualify for one. With interest rates at historic lows, the direction they are likely to go is up. Although these mortgages offer the lowest interest rate, they’re also the riskiest, as the monthly payment can increase to an amount that may prove difficult to meet. Selecting a shorter loan term, such as 15 years, can help lessen this risk.

Remember, when it comes to taking on debt, the loan amount you qualify for and the amount you can comfortably afford to repay may not be one and the same. Be sure to consider your special circumstances before taking on debt to buy a home or make another major purchase.

Savings. A standard recommended savings rate is 10 percent of gross income, but your guideline should depend on your age, goals, and stage of life. For example, as retirement nears, you may need to ramp up your savings to 20 percent or 30 percent of your income. Taking full advantage of tax-deferred retirement savings and employer match programs are almost always good ideas. Direct deposits, automatic contributions to retirement accounts, and electronic transfers from checking accounts to savings accounts can help you make saving a habit.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.

Allen Insurance and Financial was recently named as one of the 2020 Best Places to Work in Maine. This is the company’s ninth consecutive year on the list.

The awards program was created in 2006 and is a project of the Society for Human Resource Management – Maine State Council and Best Companies Group. Partners endorsing the program include: Mainebiz, the Maine State Chamber of Commerce and Maine HR Convention.

This statewide survey and awards program was designed to identify, recognize and honor the best places of employment in Maine, benefiting the state’s economy, its workforce and businesses. The 2020 Best Places to Work in Maine list is made up of 84 companies in three size categories: small (15-49 U.S. employees), medium (50-249 U.S. employees) and large (250+ U.S. employees). With 70 employee-owners, Allen Insurance and Financial is in the medium size category.

Companies from across the state entered the two-part process to determine the Best Places to Work in Maine.The first part consisted of evaluating each nominated company’s workplace policies, practices, and demographics. This part of the process was worth approximately 25% of the total evaluation.

The second part consisted of an employee survey to measure the employee experience. This part of the process was worth approximately 75% of the total evaluation. The combined scores determined the top companies and the final rankings. Best Companies Group managed the overall registration and survey process in Maine and also analyzed the data and used their expertise to determine the final rankings.

Allen Insurance and Financial will be recognized in the Oct. 19 edition of Mainebiz where the rankings will be released for the first time.

Sadly, boating season will come to an end soon, and Old Man Winter will be paving the way for snowmobiles. Winter storage for boats takes some careful planning. If you follow a checklist, winterizing your boat can be easy, ensuring your boat will be in great shape come spring.

For safe winter storage for your boat, follow our checklist:

Inspect for damage.

Thoroughly inspect the boat for any damage. Repair now, if possible.

Check electrical systems and appliances to make sure they are functioning properly (make repairs before storing the boat, if possible).

Check the battery to make sure it is fully charged before storing.

Prep the fuel system.

Fill the fuel tank but leave enough room for expansion.

Treat the fuel with a stabilizer, then run the engine for 10 minutes to get it circulating throughout the engine.

Seal the fuel valves.

Winterize the engine.

Change the oil and replace filters.

Flush the engine with fresh water, then let it drain.

Wash the engine with soap and water. Rinse thoroughly.

Fog the engine cylinders with an aerosol fogging solution.

Lubricate the engine’s grease fittings.

Flush the cooling system.

Drain any remaining coolant.

Run a less toxic propylene glycol antifreeze through the system.

Clean inside and out.

Clean the boat inside and out, removing any plant life or barnacles.

Remove any valuables from inside the boat.

Take out any food or drinks.

Bring home any cushions and store them in a cool, dry place.

Store your boat.

Remove the battery and store it in a safe, dry spot.

Consider purchasing a dehumidifier for the storage area to help prevent mildew.

Lock your boat (and leave a key with the marina manager, if applicable).

Cover and store your boat.

Check your boat periodically or have the marina check it and report to you.

Then, when spring comes around, make sure you have the right protection for your boat. Talk to an Allen Insurance representative about boat insurance.

Original Medicare, Parts A & B, travel with you, no matter where you go in the U.S.

On the other hand, Medicare Part C (advantage plans) and Medicare Part D (drug plans) don’t travel so well – you will want to make sure your plans will work for you in your new service area.

If you have moved from one state to another, you are eligible for what the Centers for Medicare and Medicaid Services (CMS) calls a Special Election Period. This SEP typically lasts two months but we recommend quick action to be sure costs you incur are covered when you need them to be.

Questions? Ask Allen. We’re here to help. Anna Moorman and Jo-Ann Neal of Allen Insurance and Financial are licensed insurance agents specializing in Medicare and are appointed with many of the major insurers in the State of Maine to help you find a product that’s the right fit for you.

Allen Insurance and Financial is holding a series of free Medicare 101 workshops in September. All are Zoom presentations with specific meeting information provided by email.

Thursday, Sept. 10, 5 to 6:30 p.m. Register with Belfast Area Adult Education: 338-3197

Monday, Sept. 21, 5 to 6:30 p.m. Register with Five-Town Adult Ed: 236-7800 x3274

Thursday, Sept. 24, with the Bremen Public Library, 7 to 8 p.m. Rregister with Jo-Ann Neal via email: jneal(at)allenif.com.

Wednesday, Sept. 30, 5 to 6:30 p.m. Register with Medomak Valley Adult Ed: 832-5205.

Anna Moorman and Jo-Ann Neal of Allen Insurance and Financial’s Benefits Division will help answer questions, including:

What does Medicare cover?

What does Medicare NOT cover?

When can I enroll in Medicare?

What is a Medicare Advantage Plan?

What is a Medicare Supplement Plan?

What plan is best for me?

Anna Moorman and Jo-Ann Neal specialize in Medicare and will be available for a question and answer session following the presentation.

In December 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, which is changing retirement and estate planning for many. One major provision of the law affects those who inherit individual retirement accounts (IRAs). So, whether you might be inheriting an IRA or are planning on leaving one to your heirs, you should understand how the SECURE Act has changed the rules for beneficiaries. The IRA strategies discussed below could help enable a sound financial plan for a rewarding retirement—for both you and your heirs.

What’s Different for IRA Beneficiaries?

The SECURE Act changes the time frame allowed for withdrawals from an inherited IRA. As you probably know, owners of a retirement account (other than original owners of a Roth IRA) generally must withdraw a minimum amount of money every year after they reach a certain age. These withdrawals are called required minimum distributions (RMDs).

Prior to the act, individual beneficiaries were entitled to take the RMDs from an inherited retirement account over the course of their life expectancy. By choosing to stretch their RMDs over time, they could benefit from tax deferral on any growth in the account. This situation has changed. Now, per the SECURE Act, many individual beneficiaries must completely withdraw the funds in an inherited retirement account within 10 years of the original owner’s death.

Exceptions to this rule include account owners who are:

A beneficiary who inherited an IRA from someone who died before January 1, 2020

The surviving spouse of the IRA owner

A child under the age of majority (Once a child reaches maturity, however, the 10-year rule applies.)

A disabled or chronically ill individual

An individual who is not more than 10 years younger than the IRA owner

As you can see, for many beneficiaries, the new 10-year withdrawal rule could result in substantially less tax-deferred growth, as well as more taxes due on withdrawal. Fortunately, there are steps you can take to help mitigate the tax burden on these IRA beneficiaries.

IRA Strategies to Consider

To help avoid any negative consequences of the 10-year withdrawal rule, the following strategies may be useful.

Converting to a Roth IRA. Although inherited Roth IRAs are subject to the new rule, distributions remain tax free. With tax rates at historic lows, you might want to consider a Roth conversion. Converting now would mean your beneficiaries (who may be in a higher tax bracket) could potentially avoid being heavily taxed on distributions.

Refusing to accept the IRA. You can refuse or disclaim inherited assets without tax implications. A qualified disclaimer must be in writing and submitted within nine months of the IRA owner’s death. In addition, the beneficiary must not have received or exercised control over the IRA, and the IRA must pass to someone other than the person who refused it.

This strategy may work well for a surviving spouse who doesn’t need the funds in the IRA. If the IRA passes to other beneficiaries (such as children), they would avoid a larger share of assets being distributed over a single 10-year period. In this case, one 10-year period would begin upon the death of the IRA’s original owner and a second 10-year period would begin for the remaining balance of the account upon the death of the surviving spouse.

Naming a trust as beneficiary. With this option, the trustee can exercise control over when IRA distributions are made. If you named a trust as beneficiary of an IRA before the implementation of the SECURE Act, however, you should review your estate plan with an attorney. In some instances, trusts drafted before passage of the SECURE Act may now be obsolete, resulting in a distribution pattern that works against the original intent of the trust.

Paying premiums on life insurance. Depending on your insurability, you may want to explore taking a withdrawal from the retirement account and use it to pay premiums on a life insurance policy. With this strategy, the beneficiaries of your policy would be set up to eventually receive a tax-free payout. This scenario might be more advantageous than leaving your retirement account to your heirs.

Making a qualified charitable distribution. If you’re older than 70½, you’re entitled to make a qualified charitable distribution (QCD). This is a tax-free gift of up to $100,000 per year from an IRA, payable directly to a charity. QCDs may become more advantageous under the SECURE Act because IRAs might be considered a less attractive inherited asset due to the elimination of the lifetime withdrawal rule.

Revising the estate plan. Working with your attorney, you might want to revise your estate plan to take an asset-by-asset approach rather than assign assets to your heirs using a percentage. For example, you might earmark IRA assets to be distributed to minors or individuals in lower tax brackets and designate a larger proportion of nonretirement assets to those with higher incomes.

Helping Secure the Future

The changes adopted as part of the SECURE Act are complex, so it’s important to work with a tax attorney to understand them. Given the new rules that affect many individuals who will inherit an IRA, you should consider a review of your estate plan and designated beneficiaries as a priority. Although many of the SECURE Act’s changes benefit those saving for retirement, it’s wise to be aware of all the options that can help you and your heirs better prepare for the future.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.

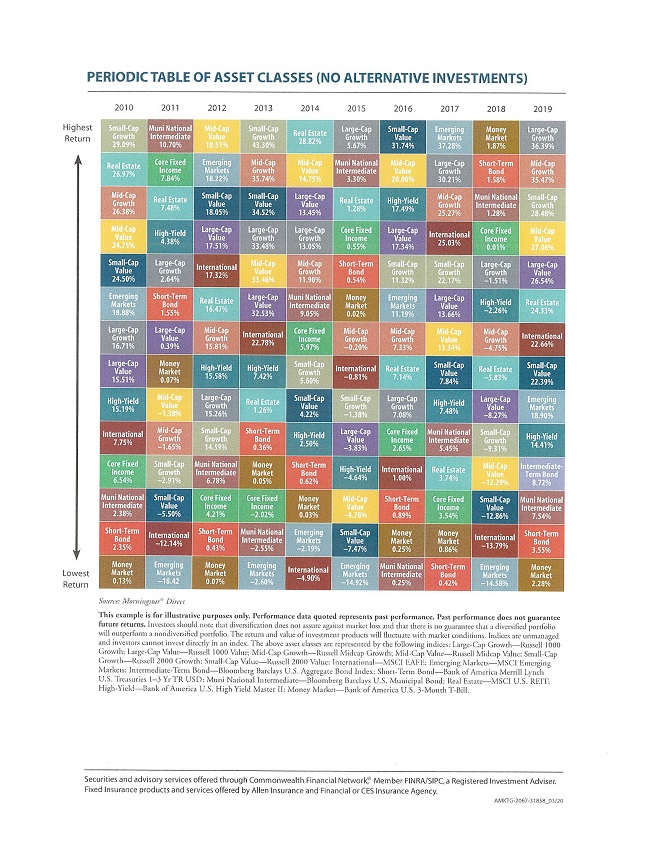

Every client has heard me talk about the keys to managing risk in their portfolios. One of those keys is diversification. This can be hard for people who are convinced they know what industry or sector is going to ‘always’ do well, so they are willing to overconcentrate there, or have stock they’ve held for a long time or received as a gift or inheritance and have grown emotionally attached or sentimental about it.

If history is a guide, then diversification is key to managing risk in a portfolio. Looking over the last 10 years, beginning with 2010 and looking at 14 recognized asset classes, like Small-Cap Growth, Real Estate, High-Yield bonds, Large-Cap Value, and their rank each year from highest to lowest return, the numbers tell the story.

For instance, some investors feel that owning large-cap growth stock is the key to their long-term success. It certainly is a strong performer but relative to the 13 other asset classes in this chart, it has been the top performer only 2 out of the past 10 years (2015 @ 5.67% and 2019 36.39%).

Small-Cap Growth has also been the top performer for 2 out of those 10 years with impressive numbers (2010 @ 29.09% and 2013 @43.3%). Ironically, Money Market was the top performer in 2018, in a year when Large-Cap Growth was 5th on the list, and Small Cap Growth was 10th. In 8 of the 10 years studied, Money Market is in the lower 7 classes out of the 14, sometimes with less than 1% performance, but never negative over those 10 years…with at least one sector performing below Money Market 7 out of 10 of those years.

Diversification can allow an investor to have at least a toe hold in as many asset classes as possible to reduce the risk that comes with investing. Some people achieve diversification by buying stocks and bonds in as many classes as feasible, although an even higher level of diversification can be achieved with mutual funds or exchange-traded funds that hold a diversified portfolio either by sector, capitalization or in the case of bonds, length of maturity, government or corporate.

These asset classes for the most part do not take into account another dimension of diversification, which is industry sector, like industrials, energy, consumer staples. Diversifying among sectors within a portfolio is also a layer of this strategy to reduce the likelihood that one sector’s underperformance will disproportionately impact the performance of a portfolio.

In 2020, during the first half of the year, looking at the 11 sectors of the S&P 500, technology stocks outperformed the other sectors at 15%, while energy underperformed the sectors and -35.3% according to Fidelity, https://www.fidelity.com/viewpoints/investing-ideas/quarterly-sector-update. The average performance of all the sectors in the S&P 500 was -3.1%. Contrast 2010, when energy performed at 20.46% and technology at 10.22% according to Invesco, https://www.invesco.com/pdf/U-SPSECTOR-FLY-1.pdf.

In conjunction with your financial advisor, in addition to defining goals and risk tolerance, consider a level of diversification that aligns with both. Having exposure in many asset classes and sectors can help a portfolio weather the volatility that can negatively impact value.

Thomas C. Chester, a financial advisor at Allen Financial in Camden, has earned the designation of Certified Plan Fiduciary Advisor from the National Association of Plan Advisors.

The Certified Plan Fiduciary Advisor (CPFA) credential — developed by some of the nation’s leading advisors and retirement plan experts — demonstrates knowledge, expertise and commitment to working with retirement plans.

Plan advisors who earn their CPFA demonstrate the expertise required to act as a plan fiduciary or help plan fiduciaries manage their roles and responsibilities.

Chester has been with Allen Financial since 2005. He has FINRA Series 6, 7, 63, and 66 registrations and he is a CERTIFIED FINANCIAL PLANNER™ Professional and Accredited Investment Fiduciary®.

Wind energy is poised to eventually be the dominant source of power in the United States.

Wind energy is poised to eventually be the dominant source of power in the United States.

Sadly, boating season will come to an end soon, and Old Man Winter will be paving the way for snowmobiles. Winter storage for boats takes some careful planning. If you follow a checklist, winterizing your boat can be easy, ensuring your boat will be in great shape come spring.

Sadly, boating season will come to an end soon, and Old Man Winter will be paving the way for snowmobiles. Winter storage for boats takes some careful planning. If you follow a checklist, winterizing your boat can be easy, ensuring your boat will be in great shape come spring.