Allen Insurance and Financial has been named one of the Best Places to Work in Maine. This is the company’s 11th consecutive year on this list.

“Best Places results are based largely on the feedback of our employee-owners – what they have to say about our company. All of us have worked hard to maintain our place on the list for the past decade but given the personal and professional challenges we have all faced over the past couple of years, these results are more important, and gratifying, than ever,” said Michael Pierce, company president.

This statewide survey and awards program is designed to identify, recognize and honor the best places of employment in Maine, benefiting the state’s economy, its workforce and businesses. The Best Places to Work in Maine list is made up of companies in three size categories: small (15-49 U.S. employees), medium (50-249 U.S. employees) and large (250+ U.S. employees). With its 90 employee-owners, Allen Insurance and Financial is in the medium size category.

Companies from across the state entered the two-part process to determine the Best Places to Work in Maine. The first part consisted of evaluating each nominated company’s workplace policies, practices, and demographics. This part of the process was worth approximately 25% of the total evaluation.

The second part consisted of an employee survey to measure the employee experience. This part of the process was worth approximately 75% of the total evaluation. The combined scores determined the top companies and the final rankings. Best Companies Group managed the overall registration and survey process in Maine and also analyzed the data and used their expertise to determine the final rankings.

Allen Insurance and Financial will be recognized in the Oct. 17 edition of Mainebiz where the 2022 rankings will be released for the first time.

“We participate in the Best Places program because it helps us learn from our employees. This feedback is invaluable because it helps us identify where we excel, and, most importantly, where we can improve,” said Pierce.

After being an avid reader of Workboat for many years it’s my distinct honor to be joining my colleague Chris Richmond as a contributor to the monthly “Insurance Watch” column. For my first go around I figured it makes sense to start with revisiting a basic topic: How to read your insurance policy.

Once you get past various legal notices, billing options and marketing messages, insurance policies have five parts: Declarations, insuring agreements, conditions, exclusions and endorsements. The smart mariner will take the time to review each of these in order, as they define the rights and responsibilities that come with the coverage you purchase.

Declarations. This is the what, where, when, by whom and for whom, price and coverage period of the policy. Check to make sure the named insureds are correct, any lenders are shown and that the right coverage lines are in place.

Insuring agreements. These explain the coverage you’ve bought in detail. An “open perils” policy covers everything except those areas covered in the exclusions (more on that below) while a “named perils” policy is for a list of specific things. Depending on the appetite of the insurer, certain additional perils can be agreed to and listed, usually by endorsement (again, more on this below).

Conditions. The insurer uses this section to outline what you must do to collaborate with them and in turn what they will do to help you get paid or to defend you in the event of a loss. This section also lays out how to file a claim. Pay close attention to the conditions, ideally before you are scrambling to file a claim, as following the ‘rules of the road’ in the policy will expedite claims handling and ordinarily lead to a smoother resolution of any call on your insurance coverage.

Exclusions. While the word itself fits certain stereotypes of insurance, this section is actually driven by logic and common sense. You can’t deliberately sink your boat or burn your warehouse and expect to get paid, and you can’t expect your Hull and P& I coverage to respond to an automobile accident. Exclusions exist to ensure your policy remains affordable, that it covers reasonable risks associated with the appropriate operations and that exposures outside the realm of insurability aren’t subject to your policy.

Endorsements. These can be used to expand or limit coverage, either at your request or at the discretion of the insurance company. Because a policy is a contract these serve as customized amendments that allow the coverage you buy provide a better fit to your unique operations. Here’s where your agent can really earn their salt and why working with agents or brokers with marine experience can make a real difference in the coverage you call on when the chips are down.

Allen Insurance and Financial is offering a series of Medicare 101 workshops in September. We hope you can join us.

All workshops are free and open to everyone, though registration is required. All will be offered via Zoom and run from 5 to 6:30 p.m. Zoom information will be send upon registration. Here is the schedule, which is also available online at AllenIF.com/Medicare.

Tuesday, Sept. 13: Register via email with Hope Library at email hidden; JavaScript is required.

Wednesday, Sept. 14: Register with Medomak Valley Adult Education; register at msad40.coursestorm.com.

Thursday, Sept. 15: Register with Belfast Adult Education; belfast.maineadulted.org.

Wednesday, Sept. 28: Register with Medomak Valley Adult Education; register at msad40.coursestorm.com

During these workshop, Jo-Ann Neal and Anna Moorman of Allen Insurance and Financial’s Benefits Division will help answer questions, including:

What does Medicare cover?

What does Medicare NOT cover?

When can I enroll in Medicare?

What is a Medicare Advantage Plan?

What is a Medicare Supplement Plan?

What plan is best for me?

Anna Moorman and Jo-Ann Neal specialize in Medicare and will be available for a question and answer session following the presentation. Meet Anna and Jo-Ann in this YouTube video.

Wendy Byrd, an account manager on the benefits team at Allen Insurance and Financial, has earned a Group Benefits Disability Specialist designation from The Hartford School of Insurance.

“Professional development is important to all of our insurance divisions but especially so in the ever-changing field of employee benefits,” said Dan Wyman, benefits division manager.

“Disability benefits are an important part of a benefits package and can make a real difference in the lives of employees and their families. This program allows Wendy to better serve our agency’s group benefits clients,” Wyman said.

Byrd has been with Allen Insurance and Financial since 2017.

You receive an email from a website you regularly use asking you to click a link to change your password due to suspicious activity. You take a phone call from the IRS asking you to verify your bank account or social security number. You get a text saying a family member was in an accident and they need money for emergency room bills.

These requests appeal to your sense of trust and seem like legitimate things to ask of you, so there’s a good chance you’ll respond or comply. But beware; these are common social engineering scams, which are ploys to access your sensitive information or obtain money using psychological manipulation.

Educate Yourself

The best way to avoid being a victim of this type of attack is to recognize the signs and know how to protect yourself. Here are the most common social engineering scams:

Phishing, smishing, vishing. These words may sound like nonsense, but they’re all widely used ways to trick you into giving away your personal information. Phishing occurs when a scammer sends you an email with a seemingly legitimate link to click, such as an email requesting a password change. Once you click and enter your password, bank account number, or other sensitive information, scammers receive access—and you might not even realize it. Smishing is a similar scam via text, and vishing is via phone or voicemail.

Protect yourself. Don’t click links from someone you don’t know, or even from an organization that might look legitimate. Go to the actual website and reach out using their posted contact information. Similarly, if someone calls you out of the blue and requests information, tell them you’ll call their organization back using a verified number. If you call the IRS, for example, they’ll likely tell you it wasn’t actually their representative calling to solicit information from you. If you receive a text and don’t recognize the sender’s phone number, don’t respond, even if the text indicates it’s from someone you know.

Baiting or quid pro quo. As the term suggests, this method offers some form of bait to tempt you into divulging information or handing over money. It could be physical bait, such as a flash drive that seems legitimate, or digital bait, such as an enticing advertisement to click or a music download. In reality, these drives or links infect your computer with malware or direct you to unsecure websites.

Quid pro quo uses a similar tactic whereby the scammer offers a service or monetary incentive in exchange for your information.

Protect yourself. Simply stated, don’t take the bait. Remain suspicious of any link or ad sent to you. If you’re interested in finding out more, you can always Google the company or product and find their official contact information. Don’t insert flash drives into your computer if you don’t know for certain what is on them or who has had access to them before you. Be wary of anyone requesting personal information, passwords, or login credentials from you, even if they claim to be an IT specialist or government official. Verify a person’s identity before responding to a request.

Piggybacking or tailgating. To carry out this type of attack, the perpetrator will try to gain physical access to a restricted space or device by following an authorized person. Think about a delivery driver asking you to hold a door open so they can deliver a package to someone in the building or an innocent-seeming stranger at a coffee shop asking to borrow your phone or laptop to look up information. Once given access, the scammer can steal your private information in a short amount of time.

Protect yourself. Get in the habit of politely declining requests like these. You might want to be helpful and accommodating, but those are the precise traits attackers seek to exploit. You can always offer to look up directions or a phone number yourself, rather than allowing someone access to your device. And you can tell the delivery driver to phone the package recipient to gain entry to the office. Don’t be the person who falls for the trick just because you were trying to be kind to strangers.

Scareware. Social engineering scams aim to make you act quickly based on emotion, and this form of attack does exactly that. You’re working on your laptop and suddenly see a pop-up warning you that your computer has multiple viruses. It instructs you to download software immediately to protect your personal information and files. This is how they put the scare in scareware. It’s natural to click as quickly as possible to prevent the issue from worsening; however, by doing so, you’ve exposed your computer to the malware you were trying to avoid.

Protect yourself. First, be sure to install legitimate antivirus/antimalware software on your device and ensure that it’s always up to date to block pop-ups from coming through in the first place. If one does appear, allow yourself time to assess the situation and think things through before acting.

Scammers are hoping you’ll panic and react quickly, but if you pause for a moment you’ll probably be able to spot an attack. Look for misspellings, lots of exclamation points, altered logos, or unprofessional words that a software company likely wouldn’t use. If you see one of these pop-ups, don’t click it—don’t even click the “X” button to close it. Instead, close your browser window and force quit through the task manager (Ctrl + Alt + Delete on Windows).

Recognize the Tactics

Overall, the best way to stay safe from social engineering scams is to recognize these tactics, verify information and sources before acting, and avoid clicking or acting quickly based on emotion. Remain calm, evaluate the originator of any request for money or information, and don’t comply until you’re sure the request is legitimate.

Although we all have the best intentions when we set financial goals each January, a lot can happen in 12 months to cause you to veer off course. Nobody wants to arrive at the end of the year and encounter a financial mess. One great way to keep yourself on a steady path to meeting your goals is to do a midyear check so you can make any necessary adjustments before things get out of hand. Use these 10 guidelines to ensure that your spending and investing are on track—and to avoid any surprises come December.

Look over your budget. This is the most basic step you can take to keep yourself on a path to financial health. Look at your spending through the middle of the year and determine whether you’re right where you want to be, you need to cut back, or you have extra funds to spend on holiday gifts. Dozens of budgeting tools are out there to assist you in tracking your budget. Many have a digital platform where you can connect your accounts and track expenses. This pulse check provides an easy way to steer yourself back if you’ve strayed from your budget. And, if you haven’t set a budget, this could be a good time to draft one and establish goals.

Reconsider your retirement contributions. Did you receive a raise during the first half of this year? If you’re not maximizing your contributions to your 401(k), 403(b), IRA, or other retirement plan, and you have additional funds from your increased salary or bonus that allow you to contribute more, it may be worth considering a bump in your retirement allocation.

Assess tax withholdings. It’s a good idea to check you tax withholdings midyear, especially if you’ve had major life events such as a job change or significant pay increases. The IRS has many tools that can assist in determining whether your tax withholdings are appropriate.

Rebalance your investment portfolio. The volatility at the beginning of 2022 may have caused your investments to drift away from your strategy. This is a great time to look at your retirement plans and taxable accounts, rebalancing your portfolios to better align with your goals.

Adjust insurance policies, if necessary. Have you had changes in your life that would warrant additional insurance? If you haven’t gotten around to adding insurance or increasing existing policies to account for marriage, having children, starting a business, buying a house, or other life events, use this midyear check to reevaluate your insurance needs.

Take stock of employee benefits. Be sure that you know when open enrollment for benefits occurs at your company and determine whether you need to make changes to your plans. This is also a good time to check on your FSA and HSA funds, submit receipts, and plan for how to use the remaining balance so you don’t lose that money.

Review your credit report. You’re legally entitled to a free copy of your credit report every 12 months from each of the three national credit bureaus (Equifax, Experian, and TransUnion). Take advantage of that opportunity to check for fraud or mistakes so you can remedy any issues as quickly as possible.

Check your emergency fund. Unexpected expenses do come up, and it’s prudent to have an emergency fund on standby to meet them. Without this money tucked away, you may have to take cash meant for other expenses or goals, or even accrue credit card debt to pay for expenses. Most experts agree that you should have three to six months of expenses in an emergency fund. Midyear is a great time to take stock of whether you’ve sufficiently saved for unexpected costs. If you’re running a surplus on your budget, it makes good financial sense to use this surplus to ensure that your emergency fund is in good shape.

Be sure that your estate documents reflect your wishes. You likely won’t need to revise your will, trust, living will, or other estate documents, but it’s a good idea to review them annually and make sure that they still align with your desires. If you’ve experienced major life events such as marriage, divorce, or birth of a child, you may want to speak with an estate planning attorney to ensure that your documents are in good order and meet your current needs.

Set financial goals for the rest of the year. Take stock of where you started and where you are midway through the year. Six months is plenty of time for situations to change and goals to shift. If nothing has changed, ensure that you are staying on track with your initial objectives. If major changes have happened in your life, you may want to reassess your financial goals for the remainder of the year.

In 2020, a record amount of more than $471 billion was given to charity according to Giving USA, a report produced by the Giving USA Foundation in collaboration with the Lily Family School of Philanthropy at Indiana University.

The issues raised in a global pandemic, challenges to a civil society and the rule of law, climate change and record stock market value levels are believed to have contributed to this record level of giving.

In the month of June, GivingUSA produces an annual report on the prior calendar year’s giving. The report on 2021 giving was recently published and reported a record amount of $484.85 Billion in giving to charity for 2021. The same issues may have been a factor, and the overall distribution of the source of those gifts remains fairly stable: 67% of those gifts were from individuals, 9% from bequests (deceased individuals), 19% from foundations, and 4% from corporate philanthropy.

Giving growing, donor advised funds gifts included. One of the interesting observations looking historically since before the Great Recession from 2006 through 2019 pointed to growth in all charitable giving of 52% and an increase of 330% in giving through donor-advised funds, which as of 2021 represented 6% of charitable giving overall. Donor advised funds are an alternative to creating a private foundation. Donors make a contribution to an organization like a community foundation or other sponsoring charity (think Fidelity Charitable), and then advise the organization as to the grants to charities they would like the fund to make. Their relative simplicity and lower administrative cost along with favorable tax treatment make them an attractive alternative to creating foundations.

Another observation about 2021 giving is the growth of 22.8% to environmental and animal protection organizations during the pandemic years. The only area seeing a decrease in giving in 2021 was education, which was down almost 3% over 2020 giving.

Bequest giving growth outpaces giving overall. Bequest gifts grew over 5 years by almost 6%, whereas overall giving growth was just over 4% during the same time period. This could represent a part of the unprecedented transfer of wealth from the boomer generation (those born between 1944 and 1964), recently estimated to be as much as $30 trillion.

Another Forbes article highlights positive giving trends through Fidelity’s Charitable Gift Funds: “Last year (2021), Fidelity Charitable donors recommended $10.3 billion in grants to their favorite charities—which is 13% more than in 2020 and a 41% increase over pre-pandemic levels!”

This is all good news for charitable organizations, reflecting generosity and willingness to share wealth to support the work of non-profits in many areas of society. It also reminds fundraisers of how important it can be to pay attention to the methods of giving that are growing the fastest, like planned gifts through estates and tax-efficient, relatively simple donor-advised funds.

Whether you are interested in purchasing a new vessel or have owned the same boat for years chances are at some point you will need a marine survey. Depending on the circumstances and who is requesting the document the survey you receive can vary greatly.

In terms of insurance, when purchasing a new vessel you will almost always need a survey in order to get an underwriter to provide you with coverage. And don’t try to use the seller’s pre-listing survey, because the underwriter most likely will not accept it. The surveyor is working for the party paying him or her to perform inspection, and underwriters want that surveyor to be working for the client who is purchasing the boat. That is why a pre-purchase survey is in your best interest.

Also known as a condition and value survey, this will be more comprehensive and the surveyor will have your best interests and concerns in mind. You do not want surprises after you have purchased the boat and a condition and value survey will provide more detail on equipment, amenities and will provide a list of recommendations of areas that need to be addressed.

Generally, insurance companies will accept a survey that is within two years old. One thing that companies always ask is if the survey recommendations have been completed. Outstanding recs are not always a show stopper, however. Depending on the severity of the recs you may be able to delay addressing them for a while. If you do have some that are significant and could affect the safety of the vessel, see if the underwriter will still provide coverage but no navigation. You can then have insurance on your vessel while she is laid up and problems are being addressed.

Should you have an accident and the insurance company gets involved, then the adjustor will most likely request a damage survey. The surveyor becomes the eyes and ears for the insurance company and is tasked with assessing the extent of damage to the vessel and attempting to determine what happened and why. This becomes very important when the adjuster decides on the payout of the claim – because the surveyor will assist in determining if the claim is covered or not.

A fit for trip survey can be requested by an underwriter to determine if a vessel is sound enough to make a voyage from one port to another. We had a client who was in the midst of a refit. The vessel needed to travel to another yard in a neighboring state to complete the job. The underwriter wanted some reassurance that the boat was capable of making the trip, hence the call for this type of survey.

The survey is one of the most important documents that an underwriter will review for your boat. If the insurance company requests and pays for the survey, don’t expect to see the complete document. The company owns the survey and most likely will not give it to you. This can save you some money in the short run but if you want to shop your boat to other markets you will need to pay for a new survey. If you have a surveyor you like, stick with him or her. He or she will be familiar with your vessel and will be more efficient in future surveys, saving you money. And finally, have a conversation with your surveyor before they step on board your boat to make sure you are both on the same page with what you are asking them to report on because you don’t want any surprises after they are done.

Whether you’ve seen the prices at the pump, clicked on the headlines, or overheard discussions in the grocery store, you know the rising cost of gas has everyone talking. At the start of the summer driving season, the average price of regular gasoline in the U.S. reached an all-time high, surpassing $4.50 per gallon. Inflationary pressures, including strong demand, supply chain disruptions, and low inventories, have caused price spikes for many consumer goods. As the cost of filling your tank rises, you’re likely wondering which markets factors caused the spike in gasoline prices.

Costs and Taxes

Crude oil is the most important input cost for gasoline. This commodity is primarily refined into gasoline and other transportation fuels, including diesel and jet fuel. Ethanol, a fuel made from corn, is blended with crude oil to represent 10 percent of gasoline volume on average, according to the Energy Information Administration (EIA). Operating costs associated with refineries, transportation (e.g., pipelines, tankers, trucking), and gas stations, as well as federal, state, and local government taxes, contribute to gasoline prices. Differences in operating costs and taxes explain the wide range of gasoline prices across states.

Higher Gasoline and Crude Oil Prices

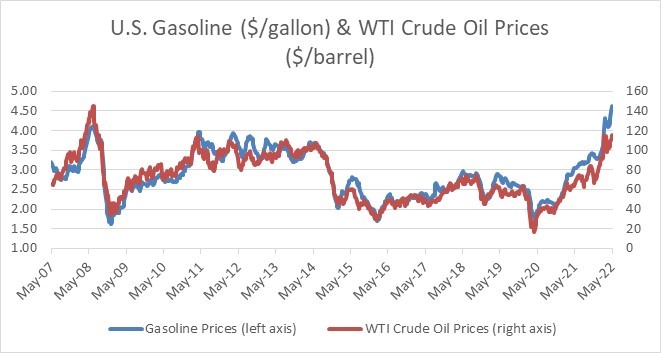

Figure 1 illustrates the strong correlation between the prices for gasoline and crude oil, which is currently around $115 per barrel for West Texas Intermediate (WTI), the U.S. index. Prices for both commodities have just about doubled since early 2021. Covid-19 lockdowns in China and plans by several countries to release strategic oil reserves helped ease oil prices in recent months. The price of gasoline, however, has continued to increase.

Figure 1. U.S. Gasoline and WTI Crude Oil Prices, 2007–2022

Source: Bloomberg

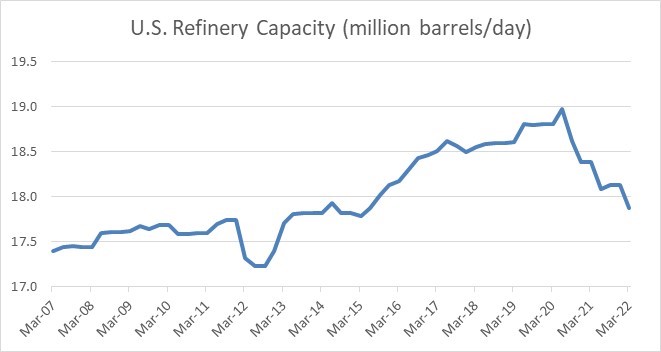

Decreased Refinery Capacity

Demand for transportation fuels, such as gasoline, dropped sharply early in the pandemic when consumers stayed home, causing several refineries to close permanently. Global refinery capacity fell in 2021 for the first time in 30 years, according to the International Energy Agency (IEA). U.S. refinery capacity dropped to 2015 levels, as shown in Figure 2. Additionally, existing U.S. refineries have limited spare capacity with utilization rates above 93 percent, the highest since December 2019. Meanwhile, refiners are generating record profits from strong demand, capacity constraints, and a higher spread between prices for oil and refined products, such as gasoline.

Figure 2. U.S. Refinery Capacity, 2007–2022

Source: Bloomberg

Lower Inventory and Higher Demand

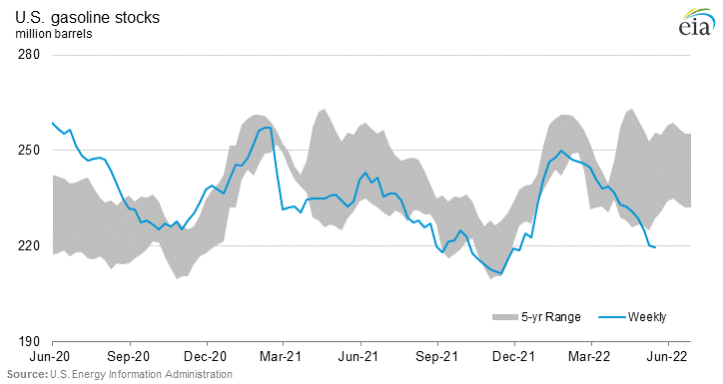

Both U.S. gasoline and oil inventories are at low seasonal levels compared to the five-year range, as shown in Figure 3, which highlights U.S. gasoline inventories. Gasoline and oil demand recovered faster than supply over the past two years while the economy bounces back from the pandemic. Refineries typically boost output before demand peaks during the summer; however, capacity constraints limit supply increases. Although the U.S. still imports oil because its refineries were initially designed to process heavy crude produced from other countries, such as Canada and Venezuela, higher U.S. exports have reduced inventories as Europe seeks to reduce its reliance on Russia for energy imports.

Figure 3. U.S. Gasoline Stocks, 2020–2022

Decline in Oil Supply

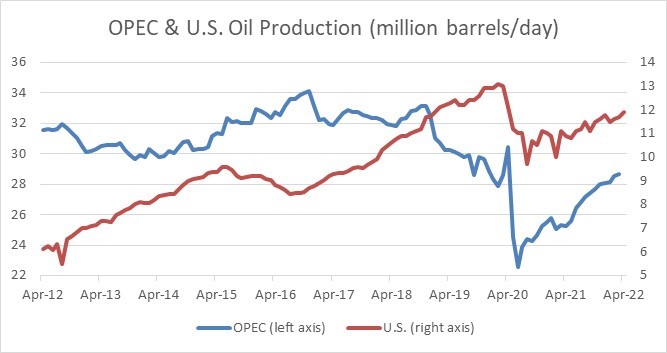

Global oil producers quickly cut capital expenditures early in the pandemic to preserve cash for debt servicing and other operating expenses amid highly uncertain oil demand and plummeting prices that fell to around $20 per barrel. Figure 4 illustrates the decline in oil production from the OPEC and the U.S., the world’s two largest groups of producers. Supply from Russia, the world’s third largest oil producing country behind Saudi Arabia, also declined after its invasion of Ukraine.

Figure 4. OPEC and U.S. Oil Production, 2012–2022

Source: Bloomberg

Oil Production Constraints

Global oil production is slowly recovering as producers have been more cautiously investing in long-term projects, such as offshore drilling, due to a highly uncertain demand outlook for oil. Traditional automakers, for instance, are investing heavily in electric vehicles amid policy support and plans by several countries to phase out internal combustion engines (e.g., gasoline, diesel) in the coming decades.

Furthermore, shareholders have forced publicly traded oil and gas producers to focus on capital discipline, profitability, reducing debt, and investor returns through dividends and stock buybacks. Production growth was the prior objective from a capital allocation standpoint, but producers struggled to generate positive cash flow and earnings following the 2014–2016 crash in oil prices.

Several other market developments have contributed to a slow recovery in oil production:

U.S. oil producers focused on drilled but uncompleted wells (DUCs) to limit costs when oil demand began to recover after the pandemic. In other words, producers sacrificed future supply growth by completing existing wells at a faster rate than drilling new wells.

A large portion of U.S. oil supply is produced from shale regions, such as the Permian Basin. Compared to conventional wells, shale wells have high depletion rates that average around 70 percent by the end of the first year, according to asset manager, GMO. This requires continuous capital expenditures to maintain or increase production levels by drilling new wells.

Small private oil producers have been the main source of production growth in the U.S. as opposed to larger publicly traded producers given shareholder demands for capital discipline.

Inflationary pressures and shortages for labor and materials, such as steel, reduced the operating capacity for oil field service companies, which supply oil rigs and other equipment to producers.

U.S. Production Forecasts

The U.S. is the world’s top oil-producing country with supply averaging 11.9 million barrels per day over the past two months. Forecasts from the U.S. EIA imply moderately higher production of about 200,000 barrels per day for the remainder of 2022. Oil production growth is expected to accelerate in 2023 and reach an all-time high, averaging more than 12.8 million barrels per day.

A Look Ahead

For the immediate future (this summer), it looks like gas and oil prices will remain high due to global supply issues, low inventories, and increased travel. There is hope for an ease or decline of prices later in the year with the potential for more supply and lower demand. Please contact my office with any questions or requests for more information on current prices or future forecasts.

###

Authored by Brad McMillan, CFA®, CAIA, MAI, managing principal, chief investment officer, at Commonwealth Financial Network®.

Colby Mank, intern at Allen Insurance and Financial, right, and Abe Dugal of Allen Financial, intern program coordinator.

Colby Mank of Union is Allen Insurance and Financial’s 2022 summer intern.

Mank is a senior finance major at Thomas College in Waterville. He plans to graduate in December.

Allen Insurance and Financial’s summer internship program creates the opportunity to learn about each of the company’s insurance and financial planning departments.

“This internship is a great opportunity for my growth as a professional,” said Mank. “The Allen team has been welcoming and encouraging – and they have so much to offer. I’m looking forward to hands-on experience in three of the areas I’ve enjoyed most at college: Investment management, marketing and risk management.”

Source: Bloomberg

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Decline in Oil Supply

Decline in Oil Supply  Source: Bloomberg

Source: Bloomberg