Allen Insurance and Financial has earned the full $10,000 Make More Happen Award from Liberty Mutual and Safeco Insurance in recognition of the agency’s ongoing support of AIO Food & Energy Assistance (AIO), a nonprofit providing low-barrier access to food, energy, and diaper assistance across Knox County.

The award initially included a $5,000 donation, with the opportunity to double it through an online campaign. Thanks to overwhelming community support, the 500-vote threshold was met, unlocking the full $10,000 for AIO’s essential programs.

“We’re incredibly grateful to our community for stepping up to help us reach this goal,” said Jill Lang, marketing director at Allen Insurance and Financial. “This donation will go a long way in supporting AIO’s work, especially during the most challenging times of the year.”

Each week, more than 450 families rely on the AIO food market, and 750 students benefit from the weekend meals program. In 2024 alone, AIO provided over 500 energy assistance gifts to help local families stay warm without sacrificing meals.

Allen Insurance and Financial has long supported AIO through fundraising, volunteerism, and outreach. This year alone, nearly 2,400 pounds of food have been collected and $39,000 raised to help sustain AIO’s vital services.

The Make More Happen Awards recognize independent insurance agencies across the U.S. for their commitment to nonprofit partners. Allen Insurance and Financial is among 36 agencies selected in 2025, with Liberty Mutual and Safeco donating up to $360,000 in total.

Picture this scenario: Your 10-year-old receives $20 for their birthday and asks, “Can we go to the store so I can buy a new toy?” As you think about how to answer, you realize this is a perfect chance to teach an important life lesson. The impulse to get something new as soon as possible is undoubtedly a strong one—in both kids and adults—but this could be an opportunity to explain the merits of saving for a larger purchase. Helping kids understand how to manage money can create habits that stick with them and help them make smart choices in the future.

Teaching children about money isn’t just practical—it’s about giving them the tools to handle life’s challenges. Early lessons about saving, spending, and planning can set them up for success.

Why Start Early?

Kids pick up habits and lessons starting at young ages, and money skills are no different. Studies show that attitudes about money are generally formed by age seven. Teaching kids while they’re young helps them build a healthy relationship with money and equips them with skills to manage it—to save, spend, and budget responsibly. These lessons can give them the tools they’ll need to avoid financial mistakes later on. In addition to helping your child make better decisions about saving, borrowing, and investing, early money lessons will help them learn to distinguish between needs and wants, a key skill for managing money wisely.

Allowance and Budgeting

An allowance is often a child’s first encounter with money, making it a great tool for teaching the basics of finance. While you may want to designate some chores as an expectation for contributing to the household (therefore, not allowance-worthy), try giving your child a weekly allowance tied to age-appropriate tasks that go beyond their expected contribution. For example, a seven-year-old might be expected to make his bed every day, but he can earn cash for changing the sheets or putting the dirty ones in the laundry.

Here’s one way to use an allowance to teach budgeting:

The three jars method: Give your child three jars labeled “Save,” “Spend,” and “Give.” Encourage them to divide their allowance among these jars. A common split is 50% for spending, 40% for saving, and 10% for giving, but you can adjust this based on your family’s priorities.

Discuss spending choices: Let them decide how to use their “Spend” money. If they want a toy, talk about whether they’ll still enjoy it a week later—in other words, is it worth the spend?

Track their money: Use a simple notebook or a basic app to keep track of allowance, savings, and spending. This helps kids see where their money is going and gain practice keeping a record of their finances.

Setting Saving Goals

Saving teaches kids patience and discipline, which can be tough when they’re naturally drawn to instant rewards. Help them set a goal for something they want, like a game or a bike, and show them how to save for it.

Set a goal together: Ask your child what they’d like to save for and figure out how much it costs. Then, break it into smaller, manageable steps. For instance, if the goal is $20 and they save $5 a week, they’ll reach it in four weeks.

Make it visual: Create a savings tracker, like a thermometer, sticker chart, or a jar they can color in as they save. This makes the process fun and the progress visible.

Celebrate success: When they reach their goal, congratulate them and tell them how impressed you are that they did it. Reinforce how saving leads to worthwhile rewards.

Introducing Investing

Investing might sound too complicated for young minds, but it can be easy for kids to understand with age-appropriate explanations.

Use familiar examples: Explain investing by comparing it to planting a seed and watching it grow. Relate it to companies they know, like ones that make their favorite toys or snacks.

Open a custodial investment account: Some financial institutions offer accounts where you can manage small investments for your child. Show them how money can grow with time and patience by explaining how the account works.

Use simple analogies: Talk about risk versus reward. For example, keeping money in a piggy bank is safe but doesn’t grow, while investing is like planting a garden—it takes time but can yield bigger rewards.

Everyday Teachable Moments

Using ordinary situations to teach money lessons helps make the concepts stick:

Grocery store shopping: Involve your child in comparing prices, discussing needs versus wants, and finding the best deals.

Family budgeting: Share how you budget for things like vacations or household expenses. Simplify it so they can understand how money is allocated.

Holiday or birthday money: If your child receives money as a gift, encourage them to split it among saving, spending, and giving.

Encouraging Generosity

Teaching kids about giving helps them develop empathy and gratitude. Suggest they donate a portion of their money to a cause they care about—like helping animals or supporting a local food bank. Explain how even a small amount can make a big difference.

A Lifelong Skill

By teaching kids about money early, you’re giving them skills they’ll use forever. Financial literacy helps them make smart decisions, avoid debt, and even build wealth. Whether it’s through an allowance, saving for a goal, or exploring investing, these lessons will prepare them for the future. Start small, keep it consistent, and watch them grow into confident, money-savvy adults.

Every parent wants to give their child the best possible future, and for many families, that includes higher education. But with tuition costs continuing to rise, figuring out how to pay for college can feel overwhelming. The good news? Starting a college fund early gives your savings more time to grow, making it easier to manage those future expenses.

529 Plans: A Popular Tool for College Savings

When it comes to saving for a child’s education, 529 college savings plans are one of the most widely used and versatile options. These state-sponsored accounts are specifically designed to help families save for qualified education expenses, and contributions grow tax free as long as they’re used for qualified expenses. Because of their flexibility and tax advantages, they’re one of the most popular ways to save for college. Begin by evaluating your state’s 529 plan, as that’s often the best place to start for state tax benefits. However, you’re not limited to your own state’s plan—you can choose almost any state’s 529 program that fits your needs.

Here’s how they work:

Contributions: Money added to a 529 plan is invested in a selection of funds or portfolios chosen by the account owner.

Growth: Earnings grow tax free, meaning you won’t owe federal taxes on the investment gains as long as the money is used for qualified education expenses.

Withdrawals: Funds can be used for tuition, fees, room and board, books, and even some K–12 tuition (in certain states) or trade schools.

Let’s say you start contributing $200 monthly when your child is born. By the time they’re 18, assuming a 6 percent annual return, you could have about $75,000 saved—and all the earnings would be tax free when used for education.

Tax Benefits

One of the biggest advantages of a 529 plan is its tax efficiency. Contributions are made with after-tax dollars, but the account’s growth and qualified withdrawals are tax free. Some states even offer tax deductions or credits for contributions, adding another layer of savings.

For example:

If you contribute $5,000 to a 529 plan in a state offering a 5% tax credit, you could save $250 on your state taxes that year.

While $250 may not seem like much, over time, these tax savings can make a meaningful difference—reducing your overall education costs just by choosing the right savings plan.

Investment Options, Age by Age

529 plans typically offer a range of investment portfolios, from aggressive growth funds to conservative options. Your child’s age and your comfort with risk will help guide your investment choices.

In the early years (ages 0–10), it often makes sense to invest more aggressively, with a higher allocation to stocks that have the potential for long-term growth. By the time your child reaches middle school (ages 11–15), gradually shifting to a more balanced approach can help manage risk. As college approaches (ages 16+), many families move to more conservative investments, such as bonds or money market funds, to help protect savings from market downturns.

Keep in mind, many plans also offer “age-based” portfolios that automatically adjust the investment mix as your child gets closer to college age.

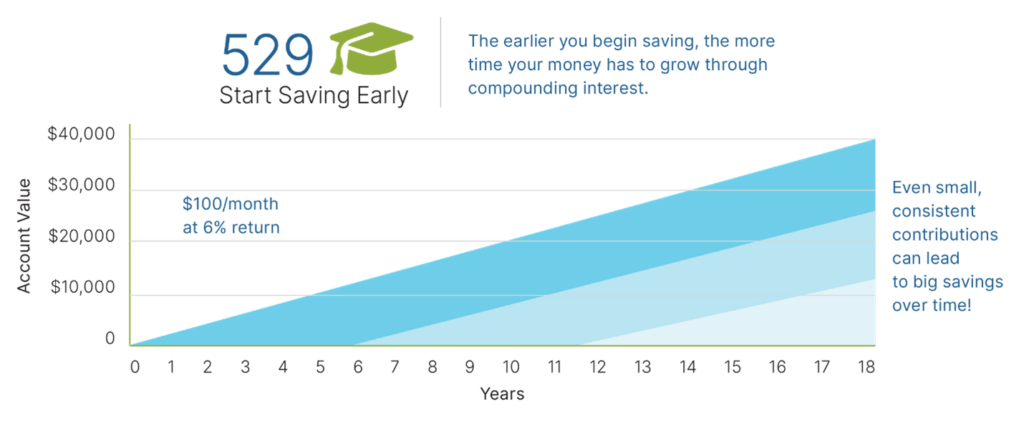

Starting Early

Time is your greatest ally when it comes to compounding growth, so it’s ideal to start as soon as possible. Setting up automatic monthly transfers often works better than trying to make larger annual contributions. For example, contributing $100 monthly feels more manageable than coming up with $1,200 at year-end. If you start contributing that $100 monthly at your child’s birth, earning an average annual return of 6 percent, you could have nearly $40,000 saved by the time they turn 18. Plus, regular contributions help you take advantage of market ups and downs through dollar-cost averaging.

Here are a few tips to get started:

Set up automatic contributions: Most 529 plans allow you to schedule recurring deposits, making it easier to stay consistent.

Start small: Even $25 a month can grow substantially over 18 years. Note that some plans do implement minimum contribution thresholds, though these are generally very low.

Gift contributions: Encourage family members, such as grandparents, to contribute to the 529 plan as part of holiday or birthday gifts. College savings works best as a family effort, with everyone pulling together toward the shared goal of providing educational opportunities for the next generation.

What If Your Child Doesn’t Pursue College? Worried about what happens if your child doesn’t go to college? 529 plans offer plenty of flexibility:

Change the beneficiary: The account can be transferred to another family member of the beneficiary, such as a sibling, cousin, grandchild, or even yourself.

Use it for other education-related expenses: Use the money for trade schools or vocational training or put it toward K–12 tuition (up to $10,000 annually, but only in certain states).

Withdraw funds: If the funds are withdrawn for nonqualified expenses, the earnings portion will be subject to taxes and a 10 percent penalty, but the principal contributions are not penalized.

Repurpose the funds: Recent changes in legislation allow up to $35,000 of unused 529 funds to be rolled into a Roth IRA for the beneficiary (subject to certain conditions).

This flexibility ensures that your savings don’t go to waste, even if plans change.

Exploring Alternatives

While 529 plans are a popular choice, they’re not the only option. Depending on your family’s circumstances, other accounts might be worth exploring:

Coverdell education savings accounts (ESAs): These accounts offer similar tax advantages to 529 plans but with lower contribution limits ($2,000 annually per child, subject to certain limits) and more flexibility in investment options.

Custodial accounts (UTMA/UGMA): These accounts allow you to save money in a child’s name, which they gain control of upon reaching adulthood. However, earnings are subject to taxes, and the funds can be used for any purpose—not just education.

Each option has unique benefits and trade-offs, so it’s helpful to compare them carefully before making a decision.

Building a Brighter Future

Starting a college fund early may seem like a daunting task but breaking it into manageable steps can help you stay on track. Whether you choose a 529 plan, a Coverdell ESA, or another option, the key is to begin as soon as you can and contribute consistently.

Saving for college doesn’t have to be overwhelming. By starting early, taking advantage of tax-advantaged accounts, and making saving a family effort, you can turn today’s small contributions into tomorrow’s opportunities—helping your child chase their dreams with confidence.

The fees, expenses, and features of 529 plans can vary from state to state. 529 plans involve investment risk, including the possible loss of funds. There is no guarantee that an education-funding goal will be met. In order to be federally tax free, earnings must be used to pay for qualified education expenses. The earnings portion of a nonqualified withdrawal will be subject to ordinary income tax at the recipient’s marginal rate and subject to a 10 percent penalty. By investing in a plan outside your state of residence, you may lose any state tax benefits. 529 plans are subject to enrollment, maintenance, and administration/management fees and expenses.

This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Liberty Mutual and Safeco Insurance have awarded Allen Insurance and Financial a 2025 Make More Happen Award for its partnership with AIO Food & Energy Assistance (AIO), a nonprofit organization that provides low barrier access to food, energy and diaper assistance with compassion and respect to households across Knox County, Maine. The award includes an initial donation of $5,000 for AIO, which can be doubled to $10,000 by having community supporters vote online.

Starting May 5, the Allen Insurance and Financial and AIO community story will be showcased on the official Make More Happen microsite at https://www.agentgiving.com/allen-insurance-and-financial, where supporters can vote to help the team reach their donation goal. If the featured story receives a mix of at least 500 votes and comments, the $5,000 donation will be increased to $10,000.

AIO plays a vital role in the community, assisting over 10% of Knox County residents in Maine. Each week, more than 450 families rely on the AIO food market, while 750 students benefit from the weekend meals program. In 2024, AIO provided 526 energy assistance gifts, easing the burden for households so they don’t need to decide between “heating or eating”. The $10,000 donation would provide food for 450 families coming to the AIO market, Weekend Meals for 750 students, diapers for 35 families, and energy payments for approximately 15 households.

“Helping to make our community a better place has always been important to our team, and AIO has given us a way to make a real difference,” said Jill Lang, marketing director at Allen Insurance and Financial. “We are grateful to Liberty Mutual and Safeco for providing much-needed funds to continue their impactful work and thrilled at the opportunity to double the donation just by calling on the community to show their support.”

Allen Insurance and Financial has supported AIO for years through volunteer efforts, fundraising campaigns and community outreach. Since 2020, the Allen team has mobilized volunteers and provided significant sponsorship each year. In 2025 alone, AIO, with the support of Allen Insurance and Financial and others in the community, has collected nearly 2,400 pounds of food and raised $39,000 in donations—enough to sustain AIO’s essential programs through the harsh winter months

“Recognizing independent agents’ dedication to their communities and nonprofit partners is what the Make More Happen Awards are all about,” said Stephanie Davis, Safeco Insurance Senior Territory Manager. “Allen Insurance and Financial is an outstanding example of how agencies can make a real difference, and we hope sharing their story inspires others to give back as well.”

Throughout 2025, Liberty Mutual and Safeco Insurance will select up to 36 independent agencies nationwide for a Make More Happen Award, donating up to $360,000 to nonprofits they support. Agencies become eligible for the award by submitting applications showcasing their commitment to a specific cause.

About Liberty Mutual Insurance

At Liberty Mutual, we believe progress happens when people feel secure. By providing protection for the unexpected and delivering it with care, we help people embrace today and confidently pursue tomorrow.

In business since 1912, and headquartered in Boston, today we are the ninth largest global property and casualty insurer based on 2024 gross written premium. We also rank 87 on the Fortune 100 list of largest corporations in the US based on 2023 revenue. As of December 31, 2024, we had $50.2 billion in annual consolidated revenue.

We employ over 40,000 people in 29 countries and economies around the world. We offer a wide range of insurance products and services, including personal automobile, homeowners, specialty lines, reinsurance, commercial multiple-peril, workers compensation, commercial automobile, general liability, surety, and commercial property.

In business since 1923, Safeco Insurance sells personal automobile, homeowners and specialty products through a network of more than 20,000 independent insurance agencies throughout the United States. Safeco is a Liberty Mutual Insurance company. You can learn more about us by visiting www.Libertymutualinsurance.com and www.Safeco.com

Mike Pierce, Debbie Tyler, Patrick Chamberlin, Jen Fifield and Chris Richmond

Hiring and onboarding play a pivotal role in establishing a strong safety culture within an organization. By carefully selecting and training new employees, businesses can significantly reduce the risk of accidents, injuries and fatalities.

While the process can seem daunting for small businesses and rote and impersonal at larger entities (and HR work can feel like a potential minefield unless a you are specialist in that area), a well thought out approach to hiring, screening, onboarding and sharing culture can pay dividends specifically in the areas of safety and the reduction of workplace injuries and more generally enterprise-wide.

The first step is to know what you are looking for in a candidate from a safety perspective. Although labor markets continue to be tight, resist the temptation to lower your standards as that marginal candidate might be the one who blows up your workers compensation or P&I experience, or who puts that work truck into the school bus.

A thorough background check is a vital component of the hiring process, especially in industries where safety is paramount. Background checks allow you to uncover criminal records, substance abuse issues or other red flags that may pose a threat to workplace safety. This in turn mitigates the risk of workplace violence, theft or other harmful behaviors and can ensure that new hires align with the organization’s values and commitment to safety.

Obviously, you should adhere to industry-specific regulations and local laws regarding background checks – especially around access and confidentiality. There are firms that specialize in running legally compliant checks for you, so this might be a task to consider outsourcing.

Candidate criteria is the next element. Look for safety-minded individuals and prioritize candidates who demonstrate a strong commitment to safety. Given that your company is unique, ensure that potential new hires align with the organization’s safety values and culture and of course verify that candidates possess the necessary skills and experience to perform their tasks safely.

Once the job offer has been made and accepted, an effective and engaging onboarding process allows you to drive home your safety culture. A comprehensive safety orientation will introduce new employees to the company’s safety policies, procedures and emergency plans.

Job-specific safety training, tailored training for each role and emphasizing potential hazards and safety precautions, coupled with practical, hands-on training to reinforce safety knowledge and skills, can cement the elements that keep new hires safe from the get-go. Mentorship and buddy systems where you pair new hires with experienced employees to guide them through safety protocols also helps teach the greenhorn that safety is core to “the way things are done around here.” Finally, regular check-ins by supervisors allow for assessment of the new hire’s understanding of safety and allows them to address any concerns either they or the employee may have.

Not only does building safety considerations into your hiring and onboarding process make for fewer workplace injuries and less impact on your insurance, it also demonstrates to rookies and veterans alike that leadership walks the walk when it comes to ensuring the whole team can enjoy a safe workplace.

Allen Insurance and Financial has pledged $25,000 to the capital campaign to expand the Harold Alfond Cener for Cancer Care, a project made necessary by increasing patient need. “Access to high-quality cancer treatment close to home is essential, and this project will make a meaningful difference for patients and their families in our community,” said Jill Lang, marketing director at Allen Insurance and Financial. “We are sincerely proud to support this project.”

This pledge reflects Allen’s deep-rooted commitment to community well-being and support for health-related initiatives. An employee-owned company, Allen aligns its corporate giving philosophy to support organizations that enhance the health and economic vitality of their region.

Pictured here are, at left, Martha Wentworth a member of Allen’s Waterville business insurance team and Jill Lang, right, from marketing director at Allen. With them is Nicole McSweeney, Chief Marketing and Philanthropy Officer at MaineGeneral Health. The photo was taken in part of the construction zone at MaineGeneral’s Harold Alfond Center for Cancer Care.

Nick Pucello of Rockport has joined Allen Insurance and Financial as a commercial lines producer, specializing in marine insurance.

Nick holds a bachelor’s degree in small vessel operations and a master’s degree in international logistics management, both from Maine Maritime Academy. Additionally, Nick holds a 1,600-ton USCG masters license and a property & casualty insurance license in the state of Maine.

Nick’s extensive experience in the marine industry includes work as a marine supply chain and logistics manager and as a yacht and tugboat captain.

Divorce is one of life’s most challenging transitions – emotionally and financially. After years of building a shared financial life, you’re suddenly faced with untangling everything, from your finances to your future plans. Questions like, “What happens to our house? How will I manage on my own? What’s fair when dividing everything we’ve built?” are essential to address.

The good news? With a clear understanding of your options and proactive planning, you can create a solid foundation for your post-divorce life.

Dividing Assets

One of the most complex aspects of divorce is dividing your assets. It’s not just about who gets what; it’s about ensuring that you have a clear picture of your financial situation and a fair plan for moving forward.

List all assets. Start by listing everything you and your spouse own. In most cases, marital property includes assets acquired during the marriage, regardless of whose name is on the title. Certain items – such as gifts, inheritances, or assets protected by a prenuptial or post-nuptial agreement – may not be considered marital property, however. Be thorough and don’t overlook assets such as frequent flyer miles, retirement accounts, or collectibles – they may factor into the financial picture.

Understand their value. Knowing what your assets are worth is important. You might need professional help, like appraisers for property or valuations for a business. For bank accounts and investments, statements from financial institutions can provide accurate numbers.

Decide how to divide. How assets are divided depends on your state’s laws. Community property states split everything 50/50, whereas equitable distribution states divide assets fairly, though not necessarily equally. A financial advisor and attorney can help you determine what’s realistic based on your situation.

Understanding Support Obligations

Divorce often brings financial obligations such as child support or spousal support (alimony). These need to be factored into your financial plan.

Child support. If you’re paying or receiving child support, know that it’s designed to cover essentials such as housing, education, and health care. Look at how this fits into your budget – whether as an expense or income – and plan accordingly.

Spousal support (alimony). Alimony helps ensure that one spouse doesn’t face undue financial hardship. This is especially important if one partner took time out of the workforce to support the family. The duration and amount vary depending on your state, so it’s smart to consult legal and financial experts to understand your options.

Legal and Mediation Costs: Plan for the Process

Divorce isn’t just emotionally taxing – it can be expensive. Budgeting for these costs early can help avoid financial surprises.

Traditional divorce. If your case is contested, you’ll likely need an attorney. Rates vary, so ask for a clear estimate upfront.

Mediation or collaborative divorce. If you and your spouse can work together, alternative methods may save you both money and stress. These approaches are typically less expensive and give you more control over the outcome.

Rebuilding Your Financial Life After Divorce

Once the paperwork is signed, it’s time to focus on your financial future. Taking these steps can help you regain control and confidence.

Create a new budget. Your income and expenses will change – new housing costs, insurance premiums, or child-related expenses might now be part of your monthly routine. Tools like budgeting apps or a simple spreadsheet can help you keep track.

Reassess your retirement goals. Divorce can affect retirement savings, especially if you’re dividing a 401(k) or IRA. A financial advisor can help you revise your plan to ensure that you’re still on track for the future you want.

Build an emergency fund. Life after divorce can be unpredictable. Aim to save at least three to six months of expenses. This cushion can help you handle surprises and start your new chapter with more peace of mind.

Special Considerations for Women

Although divorce affects everyone, women often face unique challenges that require special attention.

Earning potential and career goals. If you’ve been out of the workforce or earning less while supporting your family, this is an opportunity to focus on rebuilding your career. Consider whether you’ll need to upskill, reenter the job market, or negotiate spousal support to bridge the gap.

Retirement savings. Wage gaps and career breaks mean women often have less saved for retirement. If you’re awarded a portion of your spouse’s retirement accounts, ensure that the funds are transferred correctly, using a qualified domestic relations order (QDRO) to avoid penalties.

Health insurance. Explore new options if you were covered under your spouse’s employer-sponsored health plan. COBRA can provide temporary coverage, but marketplace plans or employer-sponsored options may be more affordable long term.

Custodial considerations. If you’re the custodial parent, plan for child-related expenses such as day care, extracurricular activities, and school fees. Be sure that these are accounted for in your divorce agreement to prevent future disputes.

Moving Forward

Divorce marks a major life transition – but it’s also an opportunity to start fresh. With the right support and financial planning, you can navigate the challenges, reduce uncertainty, and build a stable, fulfilling future.

Remember: You don’t have to do this alone. We’re here to help you every step of the way. Whether you’re just starting the process or finalizing the details, thoughtful financial planning can help you move forward with confidence.

This material has been provided for general informational purposes only and does not constitute tax, legal, or investment advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a qualified professional regarding your situation. Commonwealth Financial Network does not provide tax or legal advice.

Brittany Morse of Belmont has joined Allen Insurance and Financial as a scanning associate in the company’s Camden office. Her previous work experience includes customer service representative for a financial firm.

Morse earned her property & casualty insurance license February 2025.

Setting Saving Goals

Setting Saving Goals